Franchising: Accounting and tax accounting of operations under a commercial concession agreement. What are royalties and lump sums

In order to represent a certain brand or use its name, you need to pay royalties. In addition, there is another type of payment - a lump-sum contribution. There are some differences between these concepts, accepting them, one should study the specifics and what they have in common. The difference between royalties and lump sums lies in the amount of their payments. If the lump-sum fee has to be paid only once, royalties should be paid continuously at certain intervals.

For most merchants who are thinking about opening their own franchising facility, the concept of "lump sum" is not entirely clear and understandable. This is not surprising, the term is borrowed from the English language, not everyone thoroughly possesses it. A lump-sum fee is the key to the success of franchising. The franchise consists of several payments, the most significant is the lump-sum payment.

It often happens that large companies resort to the services of small businesses or individuals to expand their business. This type of cooperation is mutually beneficial. The meaning of the relationship lies in the transfer by the partner, who is called the franchisor in the market conditions, the right to use its technologies, services, products and trademark to the junior partner. At the same time, a cooperation agreement is drawn up between the partners. This contract provides for a *lump-sum* (one-time initial payment) that the junior partner pays to the franchisor for the services provided to him.

In any individual case, the lump-sum contribution is calculated differently, because there are no specific limits set for it in any state document. The initial payment is always described in the cooperation agreement.

A one-time * lump sum payment * is rarely used. It is mainly used in cases where a junior partner unknown on the market creates doubts about whether he will be able to commercialize and successfully release the development. A lump-sum payment is used if it is difficult to control products released under a license. In this case, the franchisor may not receive the data necessary for the calculation.

The lump-sum payment in most cases is not just a single payment, but an ordinary advance payment. As a rule, the lump-sum payment accounts for 10-20% of the license price.

The flat rate is also a lump-sum tax, which is sometimes also called a lump-sum tax. This is a fixed fee, it is charged in amounts that do not depend on economic variables. It should be noted that *lump-sum tax* can be attributed to fixed costs, since it does not depend on the volume of production.

Lump sum and postings

Change and introduction of the amount of the established capital - which are reflected in the process of rendering services by the franchisor. The established capital is contributed by the junior partner. By providing services, the franchisor reflects the movement of postings, a contribution to the capital. The movement of wiring is accompanied by documents. The franchisor takes into account the movement of capital by providing the agreed services.

Today, the most popular and profitable way to build a business is to open a business through the purchase of a franchise. A businessman along with it receives a low purchase price of goods for business, trained staff by experienced franchisors, ongoing support and a recognizable type of service or brand. A sufficient amount of lump sum and royalties will contribute to the successful implementation of the business.

When buying a franchise, the junior associate pays a certain amount, the lump-sum fee is a significant part of the fee. The lump-sum contribution is paid once, it can be paid in installments or in one amount. Most often, licensors demand payment as soon as possible.

The concept of royalties refers to other payments. These payments must be made by the junior partner who purchased the franchise. Royalties can be a fixed amount agreed in the contract, or a percentage of the profits of the junior partner. For the successful operation of a new business, partners choose the most optimal royalty rate, which is beneficial to each of them. If the royalty rate is too high, then the profitability of the franchise will be underestimated, which may make the business meaningless. To start a business when buying a franchise, you need to pay attention to the *lump fee and monthly royalties* in order to determine whether the franchise is profitable or not, and whether it is worth starting a business with it.

Royalty rate

If the franchisor determines the lump-sum fee, then the royalty is a certain rate. *Royalty rate* - this is a certain amount, remuneration to the owner for the use of his copyright. This means that the junior partner under the contract pays for the trademark, brand and name under which he conducts an independent business and receives his income from it. It should be noted that the royalty price includes promotions, marketing costs, staff training, posting information on the franchisor's or company's website.

There are three main types of royalty calculation:

- Percentage from the brand. This type of royalty is often used in cases where the store has different markup levels for goods.

- Fixed calculation. Fixed payment, it depends on the contract. The assigned amount depends on the area of the building, the number of clients served, the cost of the franchisor's services. This type of royalty is most often used by companies that find it difficult to accurately calculate the amount of income.

- Percentage of the company's turnover. To date, this type of royalty is the most common. The junior partner pays a percentage of the turnover to the franchisor, which is previously specified in the documents.

*Royalty Franchise* is the payment of the junior partner for the property objects or technological know-how transferred to him by the franchisor. Payment is made for obtaining the right to use some items protected by copyright or patents. In franchising, royalties are the most common. In this case, compensation is charged for the fact that the junior partner has the right to use trademarks, logos, slogans that identify a particular company. Thus, the junior partner, working under a false name, attracts additional customers, while he does not need to spend money on developing and creating his own brand.

Depending on the terms in the contract, the junior partner must pay royalties under one of three widely used schemes:

- Fixed royalty.

- Percentage from the brand.

- Percentage of turnover.

* Calculations use average data for Russia

To date, Russian tax legislation does not contain any taxation features that are unique to franchising. This means that an individual entrepreneur who has entered into a commercial concession agreement, as in the case of starting his own business from scratch, can choose between the general and simplified taxation systems.

When choosing a regular (general) taxation system, an entrepreneur will pay the following taxes: personal income tax (PIT), value added tax (VAT), insurance premiums (former UST). The income that the franchisee-individual entrepreneur receives is subject to personal income tax at a rate of 13% (Chapter 23 "Income Tax on Individuals" of the Tax Code of the Russian Federation). As in other cases of doing business, this type of tax is subject to all income received by the franchisee from doing business, reduced by the amount of actually incurred and documented expenses that are directly related to the receipt of these incomes (the so-called professional tax deductions). Expenses include paid insurance premiums. What kind of deductible expenses to indicate in the declaration is determined by the taxpayer himself in the same manner in which expenses are determined for tax purposes in accordance with the chapter “Corporate Income Tax”.

The main expenses that an individual entrepreneur may incur in the process of executing a commercial concession agreement are the expenses for the state registration of the franchising agreement (including the state fee), the expenses for remuneration to the franchisor (royalties and a lump-sum fee are included by analogy with the expenses associated with production and / or sale), expenses for training the franchisee (in the event that the training fee is allocated in the contract separately from the lump-sum fee and paid separately), expenses in the form of the purchase price of goods that are purchased by the franchisee directly from the franchisor or other suppliers (but only in the event that the franchisee subsequently resells them as part of his business activities), the cost of advertising the products that the user sells or produces, the services provided to him or the work performed. Advertising costs are also often included in the amount of royalties, which is quite understandable, because the franchisor has a direct interest in stimulating the sale of products under his brand. However, if there are advertising campaigns initiated by the franchisor, the franchisee also has the right to advertise his activity in the region where he conducts it. In this case, his advertising expenses reduce the tax base.

In accordance with subparagraph 20 of paragraph 1 of Article 346.16 of the Tax Code of the Russian Federation, a franchisee on a simplified taxation system can take into account as expenses the costs of advertising manufactured or purchased and / or sold goods, works or services, a trademark or service mark. The accounting procedure is given in article 264 of the Tax Code of the Russian Federation. Advertising expenses that are not mentioned in the code are recognized in the amount of not more than 1% of sales revenue, determined in accordance with Article 249 of the Tax Code of the Russian Federation.

We repeat that it is possible to take into account such expenses only if the entrepreneur can confirm all his expenses on paper. If he does not have the necessary documents proving the amount of expenses, then the professional tax deduction will be 20% of the total income received by the recipient in the course of his entrepreneurial activity.

The franchisor's fee also includes value added tax (VAT). To do this, the user must have an invoice indicating the total amount of remuneration and the corresponding amount of VAT, which is given to him by the copyright holder. According to article 164 of the Tax Code of the Russian Federation, the VAT rate on goods and services throughout the country is 18%. However, there are certain exceptions: certain goods for children, certain food products, periodicals and books of an educational nature, as well as certain medical products of domestic and foreign production are taxed at a rate of 10%. The amount of VAT on payments to the franchisor is deducted in the usual manner, which is regulated by articles 171 and 172 of the Tax Code of the Russian Federation. The right to claim the amount of VAT arises only after the payment of the lump-sum fee. In the case of royalties, VAT can be deducted after each payment of remuneration to the right holder. Accordingly, tax deductions from the cost of other works or services that are necessary for carrying out entrepreneurial activities under a commercial concession agreement are also made in accordance with the provisions of Chapter 21 of the Tax Code of the Russian Federation.

Ready-made ideas for your business

The beneficiary - an individual entrepreneur also pays insurance premiums (previously they were called the unified social tax), which amount to 34% of wages. For some types of activities, a preferential rate of insurance premiums is available (for example, for organizations working in the field of information technology or providing engineering services, firms that employ people with disabilities, and a number of other enterprises).

If the entrepreneur prefers the simplified taxation system (STS), then in this case the interest rate on taxes will be from 6 to 15%, depending on the type of simplified taxation. An additional advantage is the absence of transfers to extra-budgetary funds if the individual entrepreneur does not have employees. The tax is levied on income received by an individual entrepreneur during the tax period in cash or in kind, less expenses used to make a profit. Expenses accepted for such a deduction are determined by the provisions of Chapter 25 of the Tax Code of the Russian Federation. The expenses of taxpayers who have chosen the simplified taxation system are recognized as expenses after their actual payment, in accordance with paragraph 2 of Art. 346.17 of the Tax Code of the Russian Federation. And in accordance with paragraph 1 of Art. 252 of the Tax Code of the Russian Federation, the income received can be reduced by expenses if the latter are economically justified, confirmed by documents that meet the requirements of the law, and produced for entrepreneurial activities to generate income. If the expenses do not meet at least one of these requirements, then it will not be possible to reduce taxable income.

In the case of individual entrepreneurs operating under a commercial concession agreement, such costs included in the cost include the cost of paying a lump-sum fee and royalties, expenses in the form of the purchase price of goods purchased from the franchisor or other suppliers, the cost of paying for training to maintain franchise business.

Individual entrepreneurs who have chosen the simplified tax system pay taxes quarterly. Thus, for the year they must make four payments: for the first, second, third and fourth quarters, respectively. Payment for the first three quarters for individual entrepreneurs under the simplified tax system must be received no later than the 25th day of the month following the reporting month (that is, no later than April 25, July 25 and October 25). And the tax under the simplified tax system for the fourth quarter of the reporting year is paid no later than April 30 of the next year. An entrepreneur can pay taxes on a receipt through Sberbank or a payment card through an IP settlement account or with the help of a client bank. The amount of tax can be reduced by the amount of fixed contributions, but not more than half. This means that an individual entrepreneur on the simplified tax system of 6% can lower the tax rate to 3%.

Ready-made ideas for your business

Since 2013, an individual entrepreneur can choose the so-called patent taxation system (PSN), which is a replacement for such regimes as simplified (STS), imputed (UTII) and agricultural tax (ESHN). It is possible to switch to the patent taxation system with a tax rate of 6% voluntarily. In addition, it can be applied simultaneously with other tax regimes. However, for its application, it is necessary that the average number of employees of the enterprise does not exceed 15 people, and the total revenue from the sale of all services and goods does not exceed 60 million rubles a year.

8 people are studying this business today.

For 30 days, this business was interested in 2496 times.

Recognized brand. More than 330 partners in Russia and the CIS. Own production according to European standards.

Ivan Tea Russia. Healing fees. Health know-how. Elixir of Life.

To the question “What is a lump-sum contribution?” can be answered literally in a nutshell - this is the cost of the franchise.

For some, this answer may be sufficient, but the more curious and inquisitive person, who is also going to buy a franchise, will not be satisfied with this simple explanation.

So what is a lump sum? How and by what parameters is it formed? Is there a difference between a lump sum and royalties? And how do they differ from each other? Why is the lump-sum fee of some franchises over a million, while others are completely absent?

Let's try to answer these questions.

The lump sum is...

The etymology of the phrase "lump contribution" in Russian business vocabulary is quite interesting.

Despite the fact that franchising in its modern form took shape in the United States, in the Russian lexicon the term that refers to the cost of a franchise in America is franchisefee(translated from English - license fee) - did not take root. Instead, we use the German term die Pauschale, which in turn is derived from the related word der Bausch in the translation meaning "thick piece of something".

Even more strange is the fact that the definition of a lump-sum contribution, as in principle, and franchising, as a type of entrepreneurial activity in general, is not in Russian legislation. However, the absence of these concepts in the civil code does not mean that franchising does not exist in our country or is not legalized at all. Franchising in Russia works, but is still regulated by a commercial concession agreement (Articles 1027-1040 of the Civil Code of the Russian Federation). In the same place, in Article 1030 of the Civil Code of the Russian Federation, it is mentioned that a commercial concession agreement may contain a clause on remuneration that the user (read "franchisee") pays to the right holder (read "franchisor") in the form of a one-time and / or periodic fixed payments (read "lump sum" and "royalties").

Thus, lump sum is a fixed amount that the franchisee pays to the franchisor under a commercial concession agreement. In practice, this means that an entrepreneur, buying a franchise and concluding an agreement with a franchisor, acquires the right to conduct business under the franchisor's trademark, using his name, technologies, standards and products.

Lump sum and royalties

As mentioned above, a commercial concession agreement provides for both one-time, one-time payments, and periodic ones. The lump sum is a one-time payment. Pay and forget. It is also called the entry fee or initial payment, as it is paid immediately after the conclusion of the commercial concession agreement. Only after the payment of a lump-sum fee does active interaction begin between the franchisor and the franchisee.

Remember, a lump sum is not the only investment in a franchise business. Investments in starting a franchise business are not limited to a lump sum. No one has canceled the purchase of equipment, the purchase of goods, the payment of staff, rent, etc. You can find out what the initial investment will be spent on by requesting this information from a franchise representative at BIBOSS.

Lump sum: postings in accounting

Like any other items of expenses and income, the payment of a lump-sum fee is reflected in the accounting and taxation of both the franchisor and the franchisee.

The rules for recording accounting transactions of parties to franchising activities are based on the provision “Accounting for intangible assets” PBU 14/2007.

Consider the system of accounting and taxation of a lump-sum contribution using the example of a company that has been developing according to the franchising system since 2006 and has more than 1000 franchised enterprises. The economic model of this franchise provides only for the payment of a lump-sum contribution in the amount of 370 thousand rubles.

By the way, it should be noted that the activity under the franchise agreement is the main one for the 33 Penguins company, therefore, the receipt of remuneration under the agreement - a lump sum - is reflected in the sales income. If franchising is not the main activity for the company, the entrance fee is reflected in operating income.

When receiving a lump-sum contribution, use accounting entries 51/62, 76, and when paying 60, 76/51.

Speaking of payment. The accounting department of the franchisee "33 Penguins" takes into account the lump-sum contribution in deferred expenses on account 97 "Deferred expenses". Further, the lump-sum contribution is attributed in equal shares to the costs of ordinary activities during the term of the contract. In the case of the 33 Penguins franchise, within 5 years.

In the future, the accounting departments of the franchisor and the franchisee interact with each other within the framework of the "Supplier-Buyer" model.

Speaking about the taxation of a lump-sum contribution, it must be borne in mind that for VAT purposes the granting of exclusive rights for use under a franchising (commercial concession) agreement is considered as the provision of services.

If the contract is concluded on the terms of subsequent payment, then VAT is charged on the amount of the lump-sum payment on the date the contract enters into force. If the commercial concession agreement provides for advance payments: a one-time payment - before the transfer of the right to use the complex of exclusive rights; periodic remuneration - before the beginning of the quarter for which it is paid.

In this case, the right holder is obliged to calculate VAT on the date of receipt of the advance payment based on its amount and the estimated rate. Then, within five calendar days, issue an invoice to the user for the advance payment received. After the transfer of the right to use the set of rights (for a one-time payment) or the end of the quarter (for periodic payments), the right holder calculates VAT on the entire amount of the remuneration due and issues an invoice to the user. The amount of tax paid from the advance is deductible.

The Seven Faces of the Lump-sum

So, in order to open a franchise business, an entrepreneur needs to pay a lump-sum fee. It would seem that everything is simple, but it was not there.

If you study the franchise offers at BIBOSS, you will notice that the size of the lump-sum fee varies from franchise to franchise - from 15 thousand to 2.5 million rubles- and sometimes not at all.

For example, no lump sum Most clothing stores operate on franchising, as well as those companies for which franchising is a way to increase the number of sales outlets for their products. The more franchised enterprises and the more goods they sell, the greater will be the volume of production, which means that profits will also increase. That is why it does well without charging a lump-sum fee from its partners.

But if you look at the franchise as a product or service, then the lump-sum fee performs the function of a price and is formed according to a certain pricing system. From this point of view,

the franchise has its own cost and markup, from which the lump-sum fee is made.

But you should also not forget about the markup on the goods - the franchise. Let's remember the most important rule of pricing - this is the provision of a product or service at the price that the buyer is ready to give, and at the same time the seller will be satisfied. The franchise is no exception. A lump-sum fee is the amount that an entrepreneur is willing to pay in order to start a business under a certain brand and with the help of a franchisor. The more he values the opportunities he acquires, the higher the lump sum becomes.

In any case, the size of the lump-sum fee is determined by the franchisor, so we suggest that you familiarize yourself with the principles for the formation of a lump-sum fee for several companies.

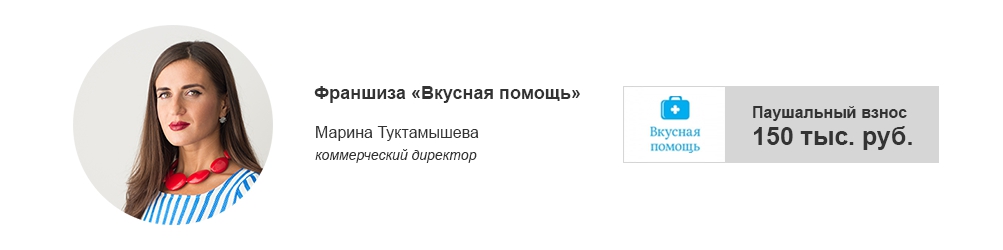

A lump-sum contribution for our company is the amount that a partner pays for using the Tasty Help brand.

The lump-sum fee of our franchise can be called enough symbolic. This amount is specified in the commercial concession agreement, which is concluded for an indefinite period.

We created a franchise not for the sake of receiving a lump-sum contribution, but to popularize our brand and increase the points of sale of our products. That is why we do not increase the lump-sum fee, are loyal to partners and are committed to long-term work.

We take the lump-sum fee as a certain degree of seriousness on the part of the franchisee - his willingness to represent the brand and grow his business with us.

The absence of a lump-sum fee is an additional advantage of the franchise offer. Without a lump sum and royalties, the franchise is more attractive and competitive in the franchise market.

Thus, the franchisee pays only for the volume of goods that is provided for by the supply agreement concluded together with the commercial concession agreement.

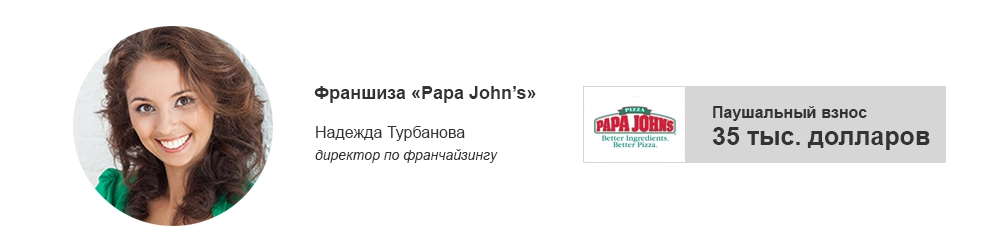

The initial fee for buying a Papa John's franchise is 35 thousand dollars. First of all, the cost of the lump-sum fee in dollars is due to the fact that PJWRI is developing Papa John's master franchise, which means that PJWRI initially agrees on the amount of the lump-sum fee, and also pays the copyright holder - the American company Papa John's - for opening each pizzeria opened by sub-franchisees. And he pays in dollars.

It is logical that we also accept an entry fee from our sub-franchisees in this currency. This is what most international companies operating on franchising in Russia do in order to protect themselves from currency fluctuations which are so common in our country.

It is worth adding that the lump-sum contribution has a special economics of miscalculation. First of all, it is related to the expected profitability of a franchised establishment.

If we consider this issue in more detail, then, first of all, a lump-sum fee is a payment for the right to work under a world-famous brand, for the technologies and recipes provided. But not only.

For example, Papa John's initial contribution paid by sub-franchisees also covers PJWRI's costs for conducting training for franchisees in Moscow, for the company's specialists to travel to open an establishment in the city of franchisees, for developing a restaurant layout and marketing plan. In addition, after payment a lump sum sub-franchisee gets ready, and most importantly, powerful sales tool- site localized for each partner.

The concept of a lump sum (amount) comes from the German expression die Pauschale(literally - a package, a large piece) and means the total cost of something, without a detailed indication of the prices of the components of the subject of the transaction. In simple words, this is the total amount of purchase for a certain amount of goods or services.

In franchising, the term lump sum refers to the cost of the direct right to enter the market under the brand name of the franchisor's company. If, however, to consider this expression from a practical point of view, we can say that this is the total price of the acquired business model of an existing company. Physically, such a payment is a single fixed amount (often rounded to the nearest whole), which can be expressed in freely convertible (dollar, euro, pounds sterling) or national currencies (rubles, hryvnia).

For what and when they pay a lump-sum payment in franchising

The initial payment is made by the franchisee one-time and only after the signing of the main contract. If the franchisor offers to deposit money before closing the deal, most likely you are dealing with an unreliable company. Many perceive a lump sum as the total cost of a finished business, but in fact this amount is a payment for a certain list of information and services, which may include:

- Brand book and the right to use the brand (trademark, trademark);

- Marketing strategy and business development program in the short term;

- Guidelines and guidelines for starting and running a business;

- Consultations of the franchisor's specialists on the selection of premises, hiring employees;

- Training of personnel and management;

- Recipes, technological maps, instructions for the production of products or the provision of services;

- Logo layouts, samples of contracts for working with clients, website templates, design projects of premises;

- Licenses and certificates;

- CRM-system and accounting software (if used);

- Bases of suppliers of raw materials, equipment.

In some cases, promotional materials and first batch products may also be provided. In turn, it is not included in the lump sum:

- The price of renting or buying premises for production and office;

- Cost of equipment and raw materials;

- Expert business support after launch (these services are paid for by royalties);

- Taxation and cost of business registration;

- Divisional advertising campaign.

Theoretically, the lump sum is a one-time payment. In other words, it is paid once in full amount. However, in practice, it can be divided into an advance (paid after the conclusion of the contract) and a residual amount (paid after the start-up of the enterprise). In the case when the amount of payment is very high, the contract may stipulate the execution of installments with the payment of several installments of the payment as the new business is opened and developed. This format gives the franchisee more guarantees, since the franchisor has an interest in the branch opening faster and starting to bring profit to the franchisee.

Another important point may be the origin of the funds contributed as a down payment. Some franchisors are skeptical about the presence of debt capital as part of such a payment.

What determines the amount of the initial payment

Each franchise has its own cost, and in some cases, the franchisor provides several options for a lump-sum fee. The amount of the latter can vary from several thousand rubles to several million. For example, one of the most expensive franchises in the world is the brand Choice Hotels International, with a lump sum of US$14.6 million.

The actual amount depends on a variety of criteria, including the following factors:

- The popularity of the franchise (trademark). The more famous the brand, the higher the cost of the business model, because in this case the franchisee is guaranteed to receive customers from the first day of work.

- The size of the opened branch. For example, store franchises can be linked to the area of the sales floor, offering business model buyers several standard options of different cost.

- Region of operation. For small towns, the lump-sum contribution may be lower, since the potential income is also lower.

- Possible risks of the franchisor. Poor-quality work of the franchisee can harm the entire franchise, and therefore the amount of the lump-sum fee initially includes possible damage.

In recent years, companies have also appeared on the franchise market offering the use of their own business model without making a lump-sum fee. They must be treated with utmost care. As a rule, in this case, two options are possible:

- The franchisor wants to advertise his product, positioning it as an opportunity to build a business with minimal start-up capital. In reality, the lump-sum payment itself can be presented in the contract as an obligation to purchase advertising materials, service or staff training.

- The franchise is just entering a new market. If a company is well known in one region, but does not yet have branches in others, it can provide more favorable conditions for franchisees, since the market, and most importantly competition, has not yet been explored, which does not allow an accurate assessment of possible development prospects and profitability.

The category of franchise without a lump-sum fee can also include programs for the development of promising managers of the franchisor's company to the level of an independent entrepreneur. In this case, the income of the parent company is formed exclusively from royalties. On the other hand, such offers are not implemented in the public domain, but are provided only to trusted partners.

How does a franchisor calculate the lump-sum fee?

If for the franchisee a lump-sum payment is the price of a package of rights, services and information, then for the franchisor it is the market value of his intellectual property, experience and labor. To determine its size, it is necessary to calculate the following parameters:

- The cost of designing a new unit (trading floor, workshop, premises in which services are provided). The easiest option is to prepare several standard projects by analogy with an existing business, having received the real cost of the work.

- Staff training costs.

- Share for the development of accounting systems, CRM, website. In this case, a certain percentage of the cost of products used by the parent company is taken, the value of which depends on the planned number of franchisees involved. For example, in order to work effectively in a given region, there should not be more than five representative offices, in this case you can put in a lump sum up to 20% of the funds you spent on purchasing the software you use.

- Franchise sale costs (advertising, presentations).

- Expected profit from the affiliate. This parameter, first of all, allows you to calculate royalties, but it is also important for determining the lump-sum contribution. It shows how interested franchisees will be in your particular model.

- License cost.

- The cost of preparing a brand book and a business plan.

- Time spent on consulting and expert assistance when launching a new division.

- Expected profit from the sale of the franchise. This amount determines how much you value your own experience and labor costs for developing a successful business model.

In addition to the nominal costs of compiling the main franchise package and the cost of basic services, when determining the size of the lump-sum fee, it is necessary to analyze its real market value, comparing it with existing similar offers from other brands.

Is it possible to return the cost of the franchise?

Since the lump-sum fee is actually a payment for the opportunity to work on the market under a certain brand, it is difficult to return it upon termination of the contract. The only way to do this is to prove that the agreement itself is invalid. This is done exclusively in court and in the presence of the following circumstances:

- The contract does not comply with existing standards and regulations established by law. For example, according to the laws of the Russian Federation, such transactions must be registered with Rospatent, and if this is not done within the established time frame, the contract will be declared invalid.

- The franchisor did not fulfill the obligations prescribed in the contract.

- The business model information provided by the franchisor is not unique and is publicly available and free of charge.

- The company selling the franchise does not own the exclusive rights to the attributes of the business model being implemented. So, it may turn out that the franchisor does not own the rights to a trademark or a unique recipe.

Legal aspects and taxation of the lump-sum contribution

In the domestic market, the purchase of a franchise is formalized as a commercial concession agreement, and from the legal point of view, the lump-sum fee is a taxable payment and subject to a tax deduction.

For the franchisor, the lump-sum payment received from the franchisee is, from the point of view of the tax code, non-operating income (unless the sale of the franchise is the main activity of the company). It is subject to VAT payable at the end of the reporting period in which the payment was received or at the time of transfer of rights to the franchisee.

If the franchisor is a foreign company, the franchisee acts as a tax agent and pays VAT, deducting it from the lump-sum fee. This applies not only to companies on the standard taxation system, but also to franchisees working on the simplified tax system.

On the other hand, if the main right holder is a taxpayer on a simplified system, then VAT is not charged from receiving a lump-sum contribution, and the payment itself is reported simply as income from activities and is subject to income tax at the previously established rate.

In order to receive a tax deduction for making a lump-sum contribution, the franchisee needs to know what intellectual property objects are included in the contract by the franchisor and whether they fall under the category of expenses on which the tax can be reduced. The latter include the following costs:

- Innovative inventions with proper patents.

- Utility models and finished industrial designs.

- PC software used in the work of the franchisee.

- Specialized databases.

- Know-how, as well as trade secrets and technologies.

Understanding the term lump sum itself, what it is in simple terms, and how it is formed from the standpoint of the franchisor and franchisee, you can always correctly assess the cost of a franchise. This will allow you both to minimize risks when looking for a suitable offer to start a business, and to ensure the optimal balance between expected profit and competitiveness when implementing your own offer.

In today's world, there are many ways to start your own business. One of the easiest is franchising. In simple terms, the concept can be interpreted as follows: someone has a unique product or technology, a trademark - that is, a certain income scheme. Such a businessman acts as a franchisor, that is, a franchise seller. The franchisee is called the franchisee. This person or enterprise, for a certain fee, receives the rights to use the technology or product. To put it simply, franchising is the rental of a trademark or a certain technology, business scheme.

The remuneration to the franchisor is carried out in the form of a lump-sum fee and royalties.

Term - lump sum

What is a lump-sum contribution? Anyone who has dealt with franchising understands that these words mean a fixed payment that is paid to the franchisor by the franchise buyer. But the phrase has many meanings, while there is no such concept in Russian legislation. And all relations in this area are regulated by the civil code, articles on commercial concession.

A lump sum appears in the lexicon of insurers and means an amount that will never be paid upon the occurrence of an insured event.

What is a franchise fee? This is a fixed amount that is paid to the franchisee when concluding a concession agreement with the franchisor.

concession agreement

In the legislation, a concession agreement means that the franchisor - the owner of a trademark or a certain method of doing business, transfers the franchisee - the buyer of this technology, the right to use for a fee, which is called royalty. In fact, there is a lease of an intellectual property object or some kind of invention, utility model - that is, something unique.

A commercial concession agreement can be safely compared with a license agreement. Only in the first version of the transaction, the conditions for using the object of the contract are described in great detail, how the franchisee's business activities will be carried out, so that the reputation of the franchisor does not suffer as a result of the actions of the latter.

Peculiarities

Due to the variety of forms of intellectual property, the contract provides for many nuances:

- limitation of territorial effect, and therefore, the place of doing business;

- urgent or perpetual nature;

- the franchisee may be subject to a requirement that limits the ability to compete with the franchisor;

- limiting the scope of the franchise;

- franchisees may be prohibited from using similar franchises acquired from others.

In addition, a commercial concession agreement may provide for a variety of ways to calculate and pay royalties, for example:

- fixed payments;

- monthly;

- disposable;

- percentage of revenue;

- margin on goods, which will be deducted to the franchisor.

Registration of the contract

The most interesting thing is that this type of transaction is subject to state registration. If the franchisor is a foreign person, then this operation is carried out by the body that registers such enterprises or individual entrepreneurs in our country.

In cases where the subject of the contract is an object that is protected by patent law, the contract must be registered by the body dealing with the regulation of relations in the field of patent law.

Partial registration of the contract may be carried out. This means that if the document contains a requirement for non-disclosure of know-how, then this part of the contract is subject to registration.

If the requirements of these rules are not met, the contract is recognized as void, that is, without any legal force.

Royalty and lump sum

The most sensitive issue when concluding a concession agreement is payments, which are of two types:

- lump sum;

- royalty.

What is a lump-sum contribution? This is the price of the franchise, the amount of which is determined by the contract and is paid only once. In fact, the payment is a payment for the acquisition of a certain technology or trademark, a kind of entrance fee.

Royalties are regular deductions. For example, for branding a catering point, a franchisee can pay 5% of the turnover of the entire establishment monthly or quarterly.

In this case, royalties are not only payments, but also additional protection for the franchise buyer. The franchisor is directly interested in the profitability of the institution, because the amount of monthly cash transfers received depends on this.

accounting entries

It is very important for both parties to the contract to understand how to correctly display expenses and income in accounting, including a lump-sum contribution. The postings and the rules for their display are specified in the provision PBU 14/2007.

If for the franchisor the sale of a franchise is the main activity, then all payments to the franchisee are displayed as part of the income from sales. When this activity is not the main one, the initial contribution is shown in operating income.

For the franchisor, the received lump-sum fee is displayed in entries 51/62, 76. Royalties - in entries 60, 76/51. If the down payment is taken into account in deferred expenses, then it is displayed on account 97 and distributed in equal parts for the entire duration of the contract.

Further relations between the franchisee and the franchisor are taken into account according to the standard scheme - "supplier-buyer".

Fixing payments in the contract

Almost any type of business transaction requires a correct description of the terms of payment. Certain financial and other conditions should also be provided for in case of non-compliance with the requirements of the contract. What it is? The lump-sum fee and royalties, the amount and terms of payment, the possible consequences of violation of the terms of the contract by any party - all this should be clearly spelled out. As a rule, payment of a lump-sum fee is a condition for starting a franchisee. If he violates the agreements, then he does not have the right to carry out entrepreneurial activities under a commercial concession agreement.

Terms of termination of the transaction and return of the initial payment

Deciding to buy a franchise can be difficult. Despite the assurances sounding from commercials and posters, the pleasure is not cheap.

What it is? A lump-sum fee must be paid, and immediately, at the conclusion of the contract. Royalties are required to be transferred monthly, in addition, you need to rent a room, purchase all related products and hire staff. Or it may happen that in a few months there will be no profit, or the franchisor is not too interested in the success of the franchisee. Therefore, it is very important to provide for the conditions for its termination even at the stage of choosing a franchise and signing an agreement.

What conditions must be provided:

- termination due to the termination of the contract;

- non-compliance with the conditions of one of the parties;

- at the initiative of one of the parties;

- if the brand that is being franchised is not registered in accordance with the procedure established by federal law;

- grounds for termination may be a court decision;

- financial insolvency of the franchisee or franchisor.

In order not to be left “overboard”, it is necessary to specify in the contract what a lump-sum franchise fee is, what it will cover. Eg:

- number of opened objects;

- what equipment and in what terms will be supplied by the franchisor;

- conditions for renting the premises, who will pay for it (possibly in equal parts or only by the franchisee);

- how the acquired technologies will be used;

- at what stage and to what extent the franchisor assists in the "promotion" of the outlet.

In fact, the agreement should cover all the details of joint business activities.

Under no circumstances should there be verbal agreements. In a situation where there will be no profit receipts, it will not be possible to prove that the franchisor has not complied with oral agreements. Do not forget that the transaction must be registered without fail. Otherwise, there can be no question of any protection of the franchisee and work in the legal field. It is very easy to cancel a transaction without registration, therefore, it is also easy to lose your investments. I would like to note that franchising and a lump-sum fee for some unscrupulous franchise sellers is all they offer. In fact, the acquisition of a franchise involves a wide range of responsibilities of the franchisor, who must actually assist in the development of the buyer's business.

How to return the initial deposit?

You should be careful when the contract is concluded on the terms of a fixed amount of royalties. As a rule, in such cases, the initial payment is quite high, and in the future the franchisor is not interested in the buyer of the brand at all. Therefore, it is most difficult to answer the question of how to return the lump-sum contribution precisely when concluding such transactions. This is most often the case with established brands that earn more from lump sums than from royalties.

Franchisees are advised to be careful and stipulate the conditions for the return of the lump-sum fee at the stage of concluding a transaction. A condition for a return may be a gross violation of its obligations by the franchisor. Eg:

- the franchisor does not have rights to the trade mark being sold;

- the seller does not deliver equipment within the agreed time frame or does not transfer business technology;

- does not provide consulting services specified in the contract, etc.

If the contract does not provide for the conditions for the return of the lump-sum contribution, then this issue can be resolved in court.

Agreement without down payment

Sometimes you can find offers - a franchise without a lump-sum fee. Is it possible? In fact, it is possible, but this does not mean that the franchisee will not have any cost part when starting a business. All expenses for rent, correspondence, telephone calls and hiring of personnel are borne by the franchise buyer. Most likely, the franchisor will have to purchase finished products or equipment. That is, the option of an agreement without a lump-sum contribution is possible, but this does not mean at all that no investments will be required or that starting a business will cost less.

Conclusion

Lump sum - what is it in simple words? This is the acquisition of a certain business technology and/or trademark. But no precautions stipulated in the contract give a full guarantee that the business will go, because entrepreneurial activity is, first of all, a risk that can be fully justified or lead to the loss of all invested funds.

- Online heart fortune telling Lenormand fortune telling what is in the heart of a loved one

- Exact signs that a man remembers or thinks about you

- Ramzan Akhmatovich biography

- Biography of Raimonds Pauls Political activities of Raimonds Pauls

- Abu Ali Ibn Sina (Avicenna) - the greatest scientist of antiquity

- Biography of Arthur Conan Doyle

- How photosynthesis happens

- The process of photosynthesis in plant leaves

- Lean system (Lean production) Number of own trainers

- Lean. Introductory course. Corporate training program for Metinvest executives What is Lean Enterprise

- Classification of the main types of losses in industrial enterprises

- How many calories in boiled carp

- Carp boiled calories per 100 grams

- Vegetable decoctions and cooking borscht, soups and cabbage soup Vegetable broth benefits

- How to cook stewed zucchini with vegetables, meat, minced meat, chicken, mushrooms?

- French beef in the oven: cooking recipes with potatoes and mushrooms French beef meat step by step recipe

- Mice in a dream are signs of a conspiracy

- Dream interpretation from a to z. Dream Interpretation: interpretation of dreams. Personal interpretation of sleep

- Fortune telling on gypsy cards “What's in the heart?

- Numerology is the square of Pythagoras: how to independently calculate the character of a person by date of birth, compatibility in love, friendship, fate, life schedule, profession, temperament, personality type, biorhythms?