Restoration of VAT previously accepted for deduction. The procedure for reflecting advances received from buyers Advances received in 1c

) on working with VAT in 1C: Accounting 8.3 (revision 3.0).

Today we will look at: “Accounting for VAT on advances received from customers.”

Most of the material will be designed for beginner accountants, but experienced ones will also find something for themselves. In order not to miss the release of new lessons, subscribe to the newsletter.

Let me remind you that this is a lesson, so you can safely repeat my steps in your database (preferably a copy or a training one).

So let's get started

We (VAT LLC) signed an agreement with Buyer LLC for the supply of goods in the amount of 150,000 rubles (including VAT).

According to the terms of the agreement, Buyer LLC must transfer to us an advance in the amount of 60% of the amount specified in the agreement, that is, 90,000 rubles.

- in the 1st quarter, LLC “Buyer”, according to the agreement, transferred us an advance in the amount of 90,000 rubles

- in the 2nd quarter we shipped goods for the entire amount specified in the contract (150,000 rubles)

It is required to formalize these transactions in the 1C: Accounting 8.3 (version 3.0) program, and also calculate VAT for each quarter.

The essence of the lesson

We will charge VAT on the advance received (90,000) in the 1st quarter, reflecting it in the sales book for the 1st quarter.

We will then charge VAT on the entire amount (150,000) in the 2nd quarter, reflecting it in the sales book for the 2nd quarter.

Finally, we will offset the VAT accrued in the 1st quarter from the advance payment (90,000), reflecting it in the purchase book for the 2nd quarter.

Total payable

- for the 1st quarter there will be VAT 90,000 * 18 / 118 = 13,728.81

- for the 2nd quarter 150,000 * 18 / 118 - 13,728.81 = 9,152.54

1st quarter

We carry out a bank statement

We enter into the program a bank statement dated 01/01/2016 for the receipt of 90,000 rubles from Buyer LLC:

Receipt to the current account will be as follows:

Please pay attention to the following points:

- type of transaction "Payment from buyer"

- a separate agreement (No. 1 dated 01/01/2016) within the framework of which settlements for this transaction will be carried out

- allocated VAT at the estimated rate (18/118)

About the settlement rate

The calculated rate (18 / 118 or 10 / 110) is used to highlight the VAT that sits within the amount.

In our case, we know that the advance is 90,000 rubles (including VAT).

We set the default VAT rate to 18%, which means that in order to get the VAT sitting at 90,000 we do a simple calculation:

90 000 * 18 / 118 = 13 728.81

The program did this calculation for us after we indicated the calculated rate of 18 / 118.

We issue an invoice for the advance payment

According to the tax code, after receiving an advance payment, we are required to issue an advance invoice to the buyer within 5 days.

Exception to this rule

According to the explanations of the Ministry of Finance, an exception can be made only for continuous long-term supplies of goods (performance of work, provision of services) to the same buyer.

For example, the supply of electricity or the provision of communication services.

For such supplies, invoicing for advances received is possible at least once a month, but no later than the 5th day of the month following the previous month.

We open processing for registering invoices for advances received:

Specify the advance search period as “1 quarter” and click the “Fill” button:

The advance received from the buyer was picked up:

But let's not rush and click the "Run" button to automatically enter the advance invoice.

First, let's pay attention to the lower part of processing with settings for the numbering and date of advance invoices:

Numbering invoices with a separate prefix "A" (from the word advance) is a rather convenient practice so that they can be easily distinguished from ordinary invoices in the purchase and sales ledger.

But there are nuances...

The tax code does not distinguish between regular and advance invoices.

And although the presence of a prefix or any other sign (sometimes accountants also write “1/AB”, “2/AB”...) is acceptable, the numbering of all invoices (both regular and advance) should be the same, for example, like this:

1, 2, A-3, A-4, 5...

When working in 1C: Accounting, we have 3 options:

- do numbering manually (many accountants often do this)

- do automatic numbering with the prefix “A” (but bad luck, then 1C will do separate numbering for invoices with and without a prefix, for example, like this: 1, 2, A-1, A-2, 3...)

- do automatic uniform numbering of all issued invoices (extremely inconvenient for an accountant)

It turns out that the first and last options fully comply with the letter of the law, but are inconvenient to work with.

The second option is convenient to use, but does not quite comply with the law.

In general, whatever one may say, few accountants have invoice numbering in perfect condition

The only consolation is that the invoice number is incorrectly indicated:

- is not a basis for refusing the buyer to deduct VAT on such an invoice

- does not entail tax and administrative liability for the seller

Registration of an invoice upon receipt of an advance means that an invoice for the advance will be registered regardless of whether the advance was credited within 5 days.

There are other options for issuing (or rather not issuing) invoices

- do not register if the advance was credited within 5 days (an indication of this possibility is in the clarification of the Ministry of Finance)

- do not register if the advance was credited before the end of the month (for supplies that fall under the clarification of the Ministry of Finance)

- do not register if the advance was credited until the end of the tax period (only for the bravest and strongest who are ready for claims from the tax authorities)

Having configured the numbering and expiration date, as in the figure above, click the “Run” button:

Let's make sure that the advance invoice has been created:

We print out the invoice in 2 copies - one for us, the other for the buyer:

- We reflected our VAT debt in the amount of 13,728 rubles 81 kopecks to the state under loan 68.02 in correspondence with debit 76.AB (VAT on advances and prepayments).

We skip the "Invoices Journal" register, it is not interesting to us (see the previous lesson).

- Write to register " VAT Sales" ensures that the advance payment is included in the sales book.

We create a sales book

We create a sales book for the 1st quarter:

And here is our invoice for the advance:

We look at the final VAT payable for the 1st quarter

There were no other business transactions in the 1st quarter, which means we can safely form the “VAT Accounting Analysis”:

VAT payable for the 1st quarter was 13,728 rubles 81 kopecks:

2nd quarter

We ship the goods

We enter into the program the sale of goods dated 04/01/2016 for LLC "Buyer" in the amount of 150,000 rubles (including VAT):

The invoice will be like this:

We analyze the postings and movements of registers...

- We wrote off the cost of goods on credit 41 accounts in correspondence with debit 90.02.1 (cost of sales). Since I didn’t actually receive the TV, the cost (the amount of wiring) turned out to be zero.

- We offset the advance payment (90,000) paid in the 1st quarter.

- We reflected revenue (150,000) for goods under credit 90.01.1 (sales revenue) in correspondence with debit 62.01 (buyer's debt to us).

- Finally, we reflected our debt (22,881.36) to the budget for VAT (credit 68.02) in correspondence with the debit 90.03 (VAT on sales).

- Write to register " VAT Sales" ensures that sales are included in the sales book.

We issue an invoice for shipment

To do this, click on the “Write an invoice” button at the very bottom of the newly created document sales of goods:

We print out the created document in two copies - one for us, the other for the buyer.

We look at the VAT payable for the 2nd quarter

We again form the “Analysis of VAT accounting” (this time for the 2nd quarter):

VAT payable for the 2nd quarter was equal to 22,881.36:

Why 22,881.36?

This is VAT on a single sale in the second quarter in the amount of 150,000 (including VAT): 150,000 * 18 / 118 = 22,881.36.

But what about the VAT already paid in the amount of 13,728.81 for the 1st quarter on an advance payment of 90,000, you ask?

And you will be absolutely right.

After all, the VAT paid on the advance in the 1st quarter should be taken into account by us when paying VAT in the 2nd quarter, when the full shipment under the contract was made, which is indicated to us by the entry in the gray box in the VAT analysis report:

Making an entry in the purchase book

To offset VAT on an advance payment, go to the “VAT Accounting Assistant”:

In the document that opens, go to the “Advances received” tab and click the “Fill in” button:

The program discovered that the advance payment on which we paid VAT in the 1st quarter was offset (a sales document for the same buyer and agreement) and now it needs to be deducted in the purchase book (otherwise we would have paid VAT on the advance payment twice):

We post the document “Creating purchase ledger entries” through the “Post and close” button:

![]()

Let's analyze the transactions and movements of the registers of the purchase ledger document...

For the curious, let’s return to the document “Creating purchase ledger entries” through the link in the VAT accounting assistant and look at its postings and movements in the registers.

- We deduct VAT on prepayments in debit 68.02 in correspondence with credit 76.AB (VAT on advances and prepayments) in the amount of 13,728.81.

- Write to register " VAT Purchases" ensures that the deduction is included in the purchase ledger.

Every accountant sooner or later encounters advance payments (whether to their suppliers or advances from buyers) and in theory knows that according to the requirements of the Tax Code of the Russian Federation (Article 154, paragraph 1; Article 167, paragraph 1, paragraph 2 ) VAT must be calculated on the advance payment on the date of its receipt. Our article today is about how to do this in practice with advance invoices in the 1C 8.3 program.

Making the initial settings

Let's take a look at the company's accounting policy and check whether the correct taxation regime is indicated: OSNO. In the “Taxes and Reports” section in the “VAT” tab, the program gives us a choice of several options for registering advance invoices (Fig. 1) (we need this setting when we act as a seller).

We may not register advance invoices in 1C if:

- the advance was credited within five days;

- the advance payment was credited until the end of the month;

- the advance was credited until the end of the tax period.

It is our right to choose any of them.

Let's analyze the offset of advances issued and advances from the buyer.

Accounting in 1C for advances issued.

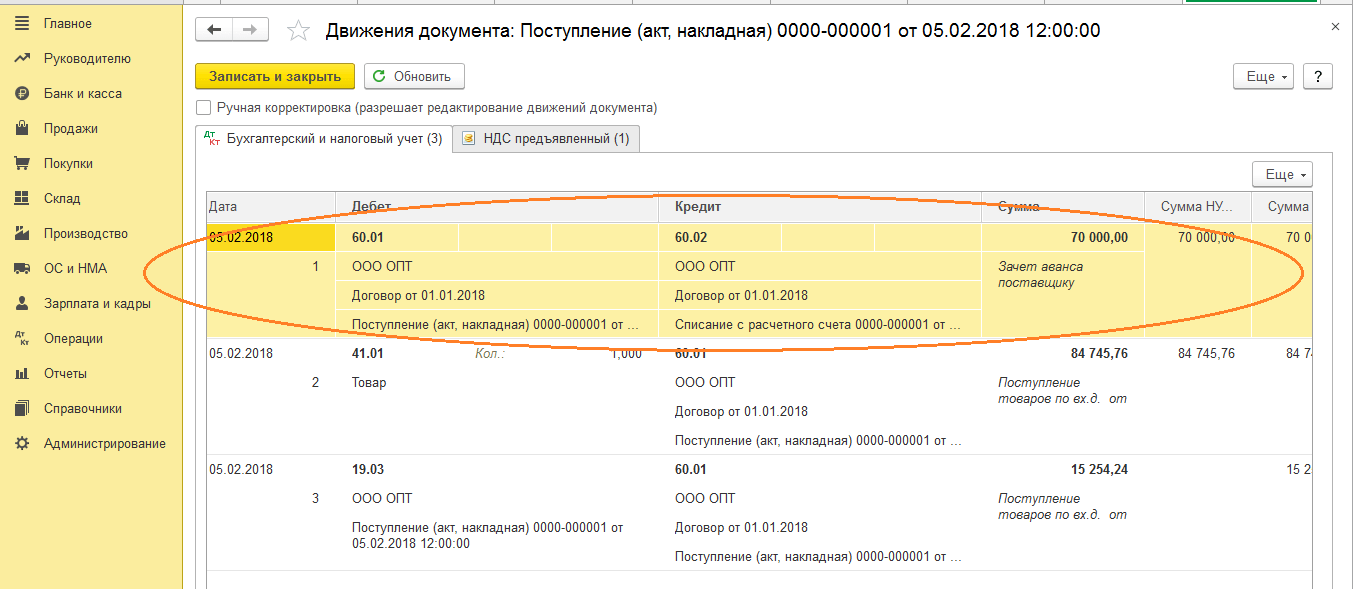

For example, let’s take the trading organization Buttercup LLC (we), which entered into an agreement with the wholesale company OPT LLC for the supply of goods. According to the terms of the contract, we pay the supplier an advance of 70%. After which we receive the goods and pay for them completely.

In BP 3.0 we issue a bank statement “Debit from current account” (Fig. 2).

Please pay attention to important details:

- type of transaction “Payment to supplier”;

- contract (when posting goods, the contract must be identical to the bank statement);

- VAT interest rate;

- offset of the advance payment with VAT automatically (we indicate a different indicator in exceptional cases);

- When posting a document, we must receive correspondence of 51 invoices with the supplier's advance invoice, in our example it is 62.02. Otherwise, an invoice for the advance payment in 1C will not be issued.

Having received payment, OPT LLC issues us an advance invoice, which we must also post in our 1C program (Fig. 3).

On its basis, we have the right to accept the amount of VAT on the advance as a deduction.

Thanks to the “Reflect VAT deduction in the purchase book” checkbox, the invoice automatically goes into the purchase book, and when posting the document, we receive an accounting entry with the formation of invoice 76.VA. Please note that the transaction type code 02 is assigned by the program independently.

Next month OPT LLC ships the goods to us, we receive them in the program using the document “Receipt of Goods”, and register an invoice. We do not correct accounts for settlements with the counterparty; we select “Automatic” for debt repayment. When posting the “Goods Receipt” document, we must receive a posting for the advance payment offset (Fig. 4).

When filling out the document “Creating sales book entries” for February, we receive automatic completion of the “VAT Restoration” tab (Fig. 5), and this amount of restored VAT ends up in the sales book for the reporting period with transaction code 22.

To reflect the final payment to the supplier, we can copy and post an existing document “Write-off from the current account”, indicating the required amount.

We create a purchase book, which reflects the amount of our VAT deduction on prepayment with code 02, and a sales book, where we see the amount of restored VAT after receiving the goods with transaction type code 21.

Accounting in 1C for advances received

For example, let’s take an organization familiar to us, LLC “Lutik” (we), which entered into an agreement with the company LLC “Atlant” for the provision of goods delivery services. According to the terms of the agreement, the buyer of Atlant LLC pays us an advance of 30%. After which we provide him with the necessary service.

The method of working in the program is the same as in the previous version.

We formalize the receipt of an advance in 1C from the buyer with the document “Receipt to the current account” (Fig. 6), followed by registration of an advance invoice, which gives us accounting entries for calculating VAT on the advance (Fig. 7).

You can register an invoice for an advance payment in 1C directly from the document “Receipt to the current account”, or you can use the processing “Registration of invoices for an advance payment”, which is located in the “Bank and cash desk” section. In any case, it immediately goes into the sales book.

At the time of the document “Sales of services”, the buyer’s advance will be credited (Fig. 8), and when the document “Creating purchase book entries” (Fig. 9) is executed, the amount of VAT on the advance received will be deducted, account 76.AB is closed (Fig. . 10).

To check the fruits of his work, an accountant usually only needs to create books of purchases and sales, as well as analyze the “VAT Accounting Analysis” report.

Work in 1C with pleasure!

If you still have questions about advance invoices in 1C 8.3, feel free to ask us on the dedicated line. They work 7 days a week and will help in the most difficult situations in tax and accounting.

For example, when products intended for sale at a rate of 18% were sold at retail, that is, without VAT. In this case, VAT on materials used in production must be restored, i.e. return to the budget. You will also have to pay VAT if the supplier’s invoice is declared invalid or lost by the tax office. The opposite situations also arise in which the organization has the right to refund previously paid VAT. In 1C, a special document is used for these purposes (Fig. 15). Fig. 15 Depending on the direction of “restoration”, the document can make adjustments either to the purchase book or to the sales book. In our example, the recovered VAT is written off as expenses (Fig. 16). Fig. 16 The amount of restored VAT is reflected in this case in the sales book, but unlike the examples discussed above, as an entry on an additional sheet (Fig. 17).

Restoring VAT in 1s 8.3 accounting 3.0

To do this, there will be an adjustment to the receipt, which is created on its basis. By default, the document is already filled out. Please note that we will recover VAT in the sales ledger. This is indicated by the corresponding flag on the “Main” tab.

Let's go to the "Products" tab and indicate what changes need to be made to the initial receipt. In our case, the number of Assorted sweets purchased changed from four to five kilograms. We entered this data in the second line “after change”, as shown in the image below.

The adjustment of the receipt, just like the initial receipt itself, made movements in two registers, reflecting only the changes made in them. Due to the fact that a kilogram of Assorted sweets costs 450 rubles, VAT on it amounted to 81 rubles (18%). It is this data that is reflected in the movements of the document.

Restoring VAT in 1s 8.3

In accordance with paragraph 3 of Article 170 of the Tax Code of the Russian Federation, the amount of VAT accepted for deduction is subject to restoration in several cases; this article will consider the restoration of VAT in 1s 8 on goods sold for export. Let's look at how to reflect this operation in the 1C Accounting program 8th edition. 2.0. VAT restoration in 1s 8 is carried out no later than the tax period in which two conditions are simultaneously met: 1.

goods were shipped for export 2. customs authorities completed customs declarations in the export mode. In our example, the enterprise purchased goods, some of which were then sold for export. After the goods arrived, VAT on them was refunded by posting: Dt 68.02 Kt 19.03. However, after these goods are sold for export, the “input” VAT on them must be restored.

How to recover VAT in 1s 8.3 accounting 3.0

That is, earlier in 1C 8.3 a VAT posting was generated: Dt 68.02 Kt 19.3. For the evening, the dishes were written off from the warehouse: Dt 91 Kt 10.3. This means that part of the VAT on previously capitalized dishes should be restored, that is, returned to the budget, since this product was not used for production purposes.

First of all, in 1C 8.3 we make an entry in the VAT recovery operation. Using the Add button, select the supplier of this product: and the invoice for which this product was received: In 1C 8.3, a complete list of all invoices received from this supplier opens. Having selected the desired invoice, add it to the list. Next, fill in all the details.

We set the amount for which VAT was restored manually based on the Write-off Certificate, that is, for what amount the dishes were released from the warehouse. For example, this is 500,000 rubles.

VAT recovery in 1s 8

Important

To reflect this operation in the 1C Accounting program 8 ed. 2.0 is intended for the document “VAT Restoration”. This document is located in the top “Purchase” menu in the “Maintaining a purchase book” section. In the new document, VAT restoration in 1s 8, we indicate that the restoration will be reflected in the sales book.

The tabular part in our example will be filled in automatically by clicking the “Fill” - “Fill in amount to be restored” button (on the panel above the tabular part). According to the document, a posting is generated: Dt 19.03 Kt 68.02 That is, the amount of VAT on those goods for which VAT was accepted for reimbursement upon receipt is restored. Sales of goods for export are carried out using a 0% rate.

To apply it, within 180 calendar days from the date of placing goods under customs export procedures, you must provide the following documents to the tax authority: 1.

How to restore VAT in 1C

Let’s say that when paying advance payments, the enterprise applied a VAT deduction, and the supplier paid or declared the amount of VAT on the advance received. To receive a deduction, the basis is the invoice issued for the advance payment. The document is issued for the amount of payment. Upon shipment, the amounts are restored from both the buyer and the supplier.

If the taxpayer did not declare the amount of VAT to be deducted, then there is no need to restore the tax. In the period when the goods actually arrive and are entered into the warehouse, the tax should be restored in the amount of the advance payment. After which you can make a deduction based on the supply invoice using the corresponding invoice. Recovering VAT from advances received When receiving an advance from the buyer, the company generates an invoice for the advance in two copies. The first is entered into the Sales Book, and the second is given to the buyer.

VAT accounting in 1s 8.3 accounting - step-by-step instructions

As a result, you will only have to pay to the budget once. Let's check that account 76.AB is closed (Fig. 10). Fig. 10 Recovering VAT from advances from suppliers Similarly, in 1C 8.3 Accounting, VAT is restored from an advance to a supplier. The document chain will look like this:

- Debiting from current account

- Invoice from supplier for advance payment

- Purchase Invoice

- Supplier invoice

Unlike the first option, “VAT restoration” will occur in the document “Creating sales ledger entries” (Fig. 11).

Fig. 11 Two entries (for advance payment and for receipt) will be created in the purchase book (Fig. 12). Fig. 12 A “restoring” entry will appear in the sales book (Fig. 13). Fig. 13 VAT on advances to suppliers is accounted for in account 76.VA. The balance on it should also be checked (Fig. 14). Fig. 14 There are a number of other moments when it is necessary to restore VAT.

VAT in 1s 8 2 in simple words

Attention

Accordingly, the VAT to be restored will be 90,000 rubles = 500,000 * 18%: If there is no invoice, let’s say the storage period has expired, then entries in the Sales Book can be made using an accounting certificate with the calculation of the amount of VAT to be restored. In 1C 8.3, VAT can be restored for all documents and transactions listed in the list that opens when filling out the document. All transactions are recorded in the same way: As a result, a posting is formed: VAT should also be restored from previously acquired or constructed real estate, which is used for non-productive purposes.

The mechanism for filling out the document is similar to the example above. Recovering VAT from advances issued How to reflect the recovery of VAT when offsetting advances issued to a supplier in 1C 8.2 is discussed using an example in the following article. VAT is restored on advances for which VAT was previously claimed for deduction.

In this article we will look in detail at how VAT is reflected when purchasing any goods, its adjustment and checking for the correctness of previously entered data. Content

- 1 Invoices

- 2 Data validation

- 3 VAT adjustment

Invoice The very first document in the chain for reflecting VAT in 1C 8.3 in our case will be the receipt of goods. The organization LLC "Confetprom" acquired 6 different nomenclature items on the basis of "Products". For each of them the VAT rate is 18%. The amount of this tax received is also reflected here. After the document was processed, movements were formed in two registers: “Accounting and tax accounting”, as well as the accumulation register “VAT presented”. As a result, the amount of VAT for all items amounted to 1306.4 rubles.

The day of confirmation of the rate is considered to be the last day of the quarter when the package of documents is collected. After confirmation of the 0% rate, the enterprise has the right to a tax deduction of “input” VAT on goods sold for export. Therefore, the amount of tax for which VAT was restored in 1C 8 can be refunded again; for more details about export operations in 1C Accounting, see the club of professional accountants. Did you like the article? Share on social media networks In accordance with paragraph 3 of Article 170 of the Tax Code of the Russian Federation, the amount of VAT accepted for deduction is subject to restoration in several cases, this article will consider the restoration of VAT in 1s 8 on goods sold for export.... .

VAT recovery in 1s step by step

Two cases of “restoration” of VAT in 1C 8.3 are shown in this illustration: In the first case, the VAT previously paid to the budget is “restored”, i.e. The VAT amount is returned to us. In the second case, we must pay the tax previously claimed for reimbursement. In both cases the same term is used, but in practice it has two directly opposite meanings.

This is especially clearly seen when analyzing VAT on advances received and paid. When we receive an advance from a buyer, an obligation arises to pay VAT on this amount. After selling the goods, we are also required to pay VAT. In order not to pay the same tax twice, we can submit the first payment for reimbursement, i.e. "restore". A similar situation, but with the opposite sign, occurs when we pay an advance to the supplier. We have the right to claim VAT on the advance payment for reimbursement, thereby reducing the total amount of tax.

In the 1C 8.3 Accounting database, VAT restoration is reflected in the VAT accounting registers. Influences the formation of the Sales Book and the Purchase Book and forms accounting entries: Dt 19 Kt 68.

The restored amount of input VAT previously accepted for deduction should be indicated in the Sales Book. To include the restored tax in the Sales Book, use invoices for which input VAT was accepted for deduction.

To reflect the VAT restoration operation in 1C 8.3, you should go to the Operations menu, then to Regular VAT operations:

Button Create – VAT Restoration:

Restoration of VAT previously accepted for deduction in 1C 8.3

Let's consider an example of VAT restoration in 1C 8.3 on goods that were used for non-productive needs of the enterprise.

Let's say an organization held a gala evening. For these purposes, utensils purchased earlier were used. When purchasing tableware with VAT, the goods were entered into the warehouse, paid, an invoice was received from the supplier and VAT was claimed for deduction in 2015. That is, earlier in 1C 8.3 a VAT posting was generated: Dt 68.02 Kt 19.3.

For the evening, the dishes were written off from the warehouse: Dt 91 Kt 10.3. This means that part of the VAT on previously capitalized dishes should be restored, that is, returned to the budget, since this product was not used for production purposes.

First of all, in 1C 8.3 we make an entry in the VAT recovery operation. Using the Add button, select the supplier of this product:

and the invoice on which this item was received:

In 1C 8.3, a complete list of all invoices received from a given supplier opens. Having selected the desired invoice, add it to the list.

Next, fill in all the details. We set the amount for which VAT was restored manually based on the Write-off Certificate, that is, for what amount the dishes were released from the warehouse. For example, this is 500,000 rubles. Accordingly, VAT for restoration will be 90,000 rubles = 500,000 * 18%:

If there is no invoice, let’s say the storage period has expired, then entries in the Sales Book can be made using an accounting certificate with the calculation of the amount of VAT to be restored.

In 1C 8.3, VAT can be restored for all documents and transactions listed in the list that opens when filling out the document. All operations are written similarly:

The result is a wiring:

It is also necessary to restore VAT on previously acquired or constructed real estate that is used for non-production purposes. The mechanism for filling out the document is similar to the example above.

Recovering VAT from advances issued

How to reflect the restoration of VAT when offsetting advances issued to a supplier in 1C 8.2 is discussed in the example

VAT is restored on advances for which VAT was previously claimed for deduction.

Let’s say that when paying advance payments, the enterprise applied a VAT deduction, and the supplier paid or declared the amount of VAT on the advance received.

The basis for receiving a deduction is: The document is issued for the amount of payment. Upon shipment, the amounts are restored from both the buyer and the supplier.

If the taxpayer did not declare the amount of VAT to be deducted, then there is no need to restore the tax.

In the period when the goods actually arrive and are entered into the warehouse, the tax should be restored in the amount of the advance payment. After which you can make a deduction based on the supply invoice using the corresponding invoice.

Recovering VAT from advances received

When receiving an advance from the buyer, the company generates an invoice for the advance in two copies. The first is entered into the Sales Book, and the second is given to the buyer.

The advance invoice after shipment is entered into the Purchase Ledger, and the new document should be reflected in the Sales Ledger as a sale. In fact, the amount is restored during the shipment period.

The amount of the advance payment received may not coincide with the material assets actually shipped. The taxpayer returns the difference or issues a new invoice for the advance payment for the amount of the excess.

How to find and correct VAT errors in 1C 8.3, mechanisms for checking VAT calculations, how to use the 1C service Reconciliation of VAT accounting data is discussed in our video:

Please rate this article:

The article discusses the procedure for registering invoices in “1C: Accounting 8” when advances are received from the buyer. 1C:ITS specialists provide options for issuing invoices for advance payments and, using a practical example, explain how to batch enter “advance” invoices for a specified period in the program using the “Registration of invoices for advance payments” processing. The setting up of the organization's accounting policy parameters regarding the procedure for registering advance invoices, as well as the numbering procedure for issued invoices, including those implemented in accordance with the explanations of the Ministry of Finance of Russia*, are discussed in detail. The information provided will help the user determine how to register advance invoices and number the invoices issued.

When an advance is received from the buyer, an organization that is a VAT payer is obliged to issue an invoice for the advance and calculate VAT.

To issue invoices for advance payments in the 1C: Accounting 8 program, there are two options for creating a document Invoice issued with invoice type For advance: together with registration of cash receipt documents (advances) and automatically (list) using processing .

Option No. 1 - together with registration of documents for receipt of funds (advances)

Funds received into the current account are registered using a document . If the funds received are an advance, then based on the document Receipt to the current account You can immediately issue an “advance” invoice.

How to issue “advance” invoices based on a document Receipt to the current account, you can read in the article “Sale of finished products in bulk (prepayment - shipment)” on ITS http://its.1c.ru/db/hoosn#content:83:2 (see operation “2.2 Issuing an invoice for advance payment "

Option No. 2 - automatically (list) using the “Registration of advance invoices” processing

This option is recommended to be used when the total number of issued invoices is large and it is necessary to automate their issuance. In this option, invoice registration can be done for one day or for an arbitrary period.

To use option No. 2, you need to set up the procedure for registering invoices for advances, adopted by the organization in its accounting policies.

Let's look at the description of option No. 2 using an example.

Example

The following business operations are performed (see table):

Setting up an organization's accounting policy

To perform operation 1 “Setting up the organization’s accounting policy” (see table), you need to go to the tab VAT specify accounting policy parameters. Setting up an accounting policy allows processing track the timing of invoices.

If there is no accounting policy for the required period, one should be created.

Change settings Accounting policies of organizations(Fig. 1):

1. Call from the menu: Company - Accounting policy - Accounting policies of organizations.

2. Select the organization and period of application of the accounting policy.

3. Click the button Change current element .

Rice. 1

Setting up a bookmark General information accounting policy (Fig. 2):

1. Set the switch General in field Tax system- in this case a bookmark appears VAT.

2. When applying UTII for some types of activities, you must check the box A special taxation procedure is applied for certain types of activities.

3. When carrying out production activities (performing work, providing services), you should check the box Production of products, performance of work, provision of services, when carrying out retail trade - checkbox Retail.

Rice. 2

Setting up a bookmark VAT accounting policy (Fig. 3):

In field Procedure for registering invoices for advance payments You can choose one of the proposed options for registering invoices for advances:

1. Always register invoices upon receipt of an advance. This option is installed in the program by default. With this option, invoices for advances received will be created for each amount received. The exception is prepayment amounts that are offset on the day of their receipt, for such received invoice amounts for advance processing Registration of invoices for advance payments are not created.

2. Do not register invoices for advances offset within 5 calendar days. With this option, invoices for advances received will be created only for those prepayment amounts that were not offset within 5 calendar days after their receipt. This option implements the rule enshrined in paragraph 3 of Article 168 of the Tax Code of the Russian Federation, according to which the seller must issue an invoice to the buyer for the amount of the prepayment within five calendar days after its receipt, if the shipment of goods (performance of work, provision of services, transfer of property rights) ) against the received prepayment is also made within the specified five days (letter of the Ministry of Finance of Russia dated March 6, 2009 No. 03-07-15/39).

3. Do not register invoices for advances credited before the end of the month. With this option, invoices for advances received will be created only for those prepayment amounts that were not credited during the month in which they were received. According to the clarifications of the Ministry of Finance of Russia, given in letter dated 03/06/2009 No. 03-07-15/39, for continuous long-term supplies of goods (provision of services) to the same buyer (supply of electricity, oil, gas, provision of communication services, etc. . p.) invoices for advances received on account of such supplies are issued to customers at least once a month, no later than the 5th day of the month following the previous month. In this case, the amount of the prepayment is determined as the difference between the payment received in the corresponding month and the cost of goods (work, services) shipped during this month.

4. Do not register invoices for advances offset until the end of the tax period. With this option, invoices for advances received will be created only for those prepayment amounts that were not credited during the tax period (quarter) in which they were received. This option is intended for organizations that are ready to resist possible claims from tax authorities regarding the timing of issuing invoices for advance payments. There is a position that payments cannot be recognized as advance payments if payment and shipment of goods occurred in the same tax period. Since the tax period for VAT is considered a quarter (Article 163 of the Tax Code of the Russian Federation), the seller should not issue invoices for advances received in the quarter in which the goods were shipped (work performed, services provided).

5. Do not register invoices for advances (Clause 13, Article 167 of the Tax Code of the Russian Federation). The option is intended for organizations whose activities fall under paragraph 13 of Article 167 of the Tax Code of the Russian Federation, i.e., which are engaged in the production of goods (work, services) (according to the list determined by the Government of the Russian Federation) with a production cycle duration of more than six months. In the case of receiving an advance payment for the specified goods (work, services), these organizations have the right to determine the moment the tax base arises as the day of shipment (transfer) of these goods (performance of work, provision of services).

One of the selected options will apply to all contracts in the organization.

If an agreement with a specific buyer has specific features, then for this agreement you can establish an individual procedure for generating advance invoices. To do this, you need to uncheck the box in the contract form Register advance invoices in a manner consistent with accounting policies and select the required element from the list (Fig. 6).

Rice. 3

Issuing an invoice to the buyer

To perform operation 2 “Issuing invoices to the buyer” (see example table), you need to create a document Invoice for payment to the buyer. The document does not generate transactions.

Creating a document Invoice for payment to the buyer(Fig. 4):

1. Call from the menu: Sale - Check.

2. Button Add .

Rice. 4

Filling out the document header Invoice for payment to the buyer(Fig. 5):

1. In the field Stock select the warehouse from which you plan to ship goods.

2. In the field Counterparty select a buyer from the directory Counterparties.

3. In the field Agreement select an agreement with the buyer. Attention! In the contract selection window, only those contracts that have the contract type are displayed With buyer(Fig. 6).

4. In the field Bank account select a bank account to transfer funds from the buyer.

Rice. 5

Rice. 6

Checkbox Register advance invoices in a manner consistent with accounting policies is removed when, for a specific contract, it is necessary to establish an individual procedure for generating invoices for advance payments, different from the accounting policy settings (see Fig. 3).

In field Generalized name of goods for an advance invoice the name of goods (works, services) is indicated (from the directory Nomenclature), which will be inserted into the “advance” invoice issued to the buyer in the absence of an invoice for payment. When issuing an invoice in the “advance” invoice, in the field Nomenclature (general name), the item specified in the invoice is transferred.

Filling out a bookmark Goods document Invoice for payment to the buyer(Fig. 7):

1. Click the button Add .

2. In the field Nomenclature select the products sold (in the directory Nomenclature The product name is usually located in the folder Goods).

3. Fill in the remaining fields as shown in Figure 7.

4. To save the document, click the button Write down.

5. To call the printed Invoice form, use the button An invoice for payment.

6. Button OK.

Rice. 7

By analogy with this document, two more invoices are created for payment to the buyer:

Receipt of advances from the buyer

To perform operation 3 “Receipt of advances from the buyer” (see example table), you need to create a document based on document Invoice for payment to the buyer. As a result of the document Receipt to the current account The corresponding postings will be generated.

Creating a document Receipt to the current account(Fig. 8):

1. Call from the menu: Sale - Check.

2. Select the base document ( Invoice for payment to the buyer).

3. Click the button Enter based on.

4. Select Receipt to the current account with document operation type Payment from the buyer . Moreover, based on the document Invoice for payment to the buyer a new document is created and automatically filled in Receipt to the current account. It is necessary to check the completion of its fields and edit them.

Filling out the document Receipt to the current account(Fig. 8):

1. In the field from indicate the date of payment according to the bank statement.

2. In the field In. number Enter the buyer's payment order number.

3. In the field In. date Enter the date of the buyer's payment order.

4. In the field Settlement account check that account 62.01 “Settlements with buyers and customers” is indicated.

5. In the field Advance account check that account 62.02 “Calculations for advances received” is indicated.

6. In the field Money movement article. funds you must select the appropriate article.

7. Fill in the remaining fields as shown in Figure 8.

Rice. 8

To post a document, click the button Conduct , to view transactions, click the button Result of the document .

Figure 9 shows the result of the document Receipt to the current account.

Rice. 9

By analogy with this document, two more documents are created Receipt to the current account:

From 05/12/2012 in the amount of RUB 1,500,000;

From 06/12/2012 in the amount of 2,000,000 rubles.

As a result of these documents, transactions will also be generated reflecting the receipt of advances from the buyer:

1. Debit 51 “Current accounts” - Credit 62.02 “Calculations for advances received” - RUB 1,500,000.00.

2. Debit 51 “Settlement accounts” - Credit 62.02 “Calculations for advances received” - RUB 2,000,000.00.

Registration of invoices for advance payment by list

To perform operation 4 “Registration of advance invoices by list” (see example table), you need to process Registration of invoices for advance payments.

Processing is intended for automatic generation of documents Invoices issued with a view For advance.

Start processing Registration of invoices for advance payments(Fig. 10):

Call from the menu: Sale - Maintaining a sales book - Registration of invoices for advance payments.

Filling out the processing header Registration of invoices for advance payments(Fig. 11):

1. In the fields Period from... to... select the period for which processing is performed.

2. Click on the hyperlink Always register invoices upon receipt of an advance. A window appears Accounting policies of organizations(see Fig. 3), in which on the tab VAT an option for registering invoices for advances is indicated.

3. Click on the hyperlink Uniform numbering of all issued invoices. A window appears Setting up accounting parameters(Fig. 12), in which on the tab VAT You can determine the numbering order of issued invoices:

- Uniform numbering of all issued invoices- all issued invoices will be numbered in chronological order sequentially, regardless of their type, in particular, “advance” invoices will not have the prefix “A”. The setting is installed by default and takes effect after updating the configuration to release 2.0.39.6. When switching to this numbering, previously issued invoices are not renumbered;

- Separate numbering of invoices for advance payments with the prefix “A”- issued invoices will be numbered in chronological order sequentially, with the exception of “advance” invoices, which have a separate numbering with the addition of the prefix “A”. This mode was used before changes were made to the accounting settings (before release 2.0.39.6).

The possibility of a single numbering of all issued invoices was implemented in connection with the clarifications of the Ministry of Finance of Russia given in letter No. 03-07-11/284 dated August 10, 2012. In it, the financial department indicated that the serial numbers of the adjustment invoice and invoice are assigned in general chronological order (clause “a”, clause 1 of the Rules for filling out the adjustment invoice, approved by Decree of the Government of the Russian Federation of December 26, 2011 No. 1137) . At the same time, separate numbering of invoices for advances is not provided for by Decree of the Government of the Russian Federation of December 26, 2011 No. 1137. Please note that the tax authorities allow the presence of additional information in invoices (letter of the Federal Tax Service of Russia dated March 12, 2012 No. ED-4-3/4061@ together with letter of the Ministry of Finance of Russia dated February 9, 2012 No. 03-07-15/17) . In particular, the number assigned in chronological order may be supplemented by a letter designation, for example the letter “A” for advance invoices. Thus, if an organization assigned invoice numbers not in chronological order, then in accordance with the norms of the tax legislation of the Russian Federation, the taxpayer is not liable for this. At the same time, in accordance with paragraph 2 of Article 169 of the Tax Code of the Russian Federation, an organization can accept VAT as a deduction.

Rice. eleven

Rice. 12

Filling out the processing tabular part Registration of invoices for advance payments(Fig. 13):

1. Click the button Fill to automatically fill out the tabular part of processing based on accounting data. When filling out the list, the balances of advances received from customers are analyzed for each date for the specified period. Amounts of advances for which the invoice registration period has not yet arrived or the invoice is not registered are not taken into account. If in an earlier period (not covered by running processing) there was an advance payment, on the basis of which an invoice was not issued, then the line with such an advance payment is also placed in the tabular part of processing and highlighted in red. The criteria for this analysis are the period selected by the user and the accounting policy settings (or the agreement with the buyer).

2. After filling out the list, you can change the field data, for example, adjust the amount of advances (field Advance amount) and etc.

3. Click the button Execute for the generation and processing of invoices for advance payments.

4. Press the button List of invoices (issued) to view the list of created invoices for the specified period (Fig. 14). Open each document to view and edit Invoice issued(Fig. 15).

Rice. 13

Rice. 14

Editing the document invoice issued (Fig. 15):

1. In the window that opens Invoice issued The document fields will be automatically filled in.

2. Checkbox Correction number is established in case of registration of a corrected invoice. In our example, corrected invoices do not appear, so there is no need to select this checkbox.

3. Field Type of invoice filled with default value For advance.

4. Field Nomenclature (general name) is filled in automatically with data from the invoice for payment (see Fig. 7) or (if there is no invoice) with data from the directory Contracts of counterparties(see Fig. 6).

5. Fields date And Number payment and settlement document are filled automatically with data from the document Receipt to the current account.

6. Field Operation type code is filled in automatically and corresponds to the code of the operation being carried out, which is displayed in column 4 Logbook of received and issued invoices.

8. Swipe the document by pressing the button Conduct.

9. To call the printed Invoice form, use the button Invoice.

10. Button OK.

Rice. 15

To view transactions generated when posting a document Invoice issued click the button Result of the document . Figure 16 shows the result of the document.

Rice. 16

Invoices issued are recorded in the journal of received and issued invoices (Fig. 17) and the sales book (Fig. 18).

You can use the menu to call the printed form of the journal Sale - Maintaining a sales book - Journal of invoices according to Decree No. 1137, this magazine can also be called up from the menu Purchase - Maintaining a purchase book - Journal of invoices according to Decree No. 1137.

Rice. 17

Creating a printed form of the sales book (Figure 18):

1. Call from the menu: Sale - Maintaining a sales book - Sales book according to Decree No. 1137.

2. In the fields Period from... to... select the period for which the book is created.

3. Using a button Settings select JSC "TF-Mega" (Fig. 19).

4. Press the button Form .

Rice. 18

- Qigong: Chinese practice of strengthening the body

- Oed Society for Children's Evangelism

- Lemon shortbread cookies How to make lemon shortbread cookies

- Yeralash salad with beef recipe

- Pink salmon baked in the oven with potatoes

- How to cook brushwood at home: delicious and easy recipes

- Homemade basturma - the best recipes

- How to arrange a desktop according to Feng Shui for money

- Conspiracies against a rival will return peace to the family

- Notes on teaching literacy in the preparatory group “Space Travel”

- Official Sergei Rybakov: “Time is what we put into it

- Environmental studies

- New leader, old leader

- Finance in economics. Banking system. Finance in economics Presentation social studies 11th grade finance in economics

- Presentation on the topic of finance in economics

- Origin and history of the Avar people

- Medical devices for treating joints at home Household ultrasonic physiotherapy device for treating joints

- Territorial unit prices

- Kronstadt uprising ("rebellion") (1921) Suppression of the Kronstadt uprising

- Taoist system. L. BingSecrets of love. Taoist practice for women and men. System "Universal Tao"